The currency may look strong but its weaknesses are mounting…

This month, as the dollar surged to levels last seen nearly 20 years ago, analysts invoked the old Tina (there is no alternative) argument to predict more gains ahead for the mighty greenback.

What happened two decades ago suggests the dollar is closer to peaking than rallying further. Even as US stocks fell in the dotcom bust, the dollar continued rising, before entering a decline that started in 2002 and lasted six years. A similar turning point may be near. And this time, the US currency’s decline could last even longer.

Adjusted for inflation or not, the value of the dollar against other major currencies is now 20 per cent above its long-term trend, and above the peak reached in 2001. Since the 1970s, the typical upswing in a dollar cycle has lasted about seven years; the current upswing is in its 11th year. Moreover, fundamental imbalances bode ill for the dollar.

When a current account deficit runs persistently above 5 per cent of gross domestic product, it is a reliable signal of financial trouble to come. That is most true in developed countries, where these episodes are rare, and concentrated in crisis-prone nations such as Spain, Portugal and Ireland. The US current account deficit is now close to that 5 per cent threshold, which it has broken only once since 1960. That was during the dollar’s downswing after 2001.

Nations see their currencies weaken when the rest of the world no longer trusts that they can pay their bills. The US currently owes the world a net $18tn, or 73 per cent of US GDP, far beyond the 50 per cent threshold that has often foretold past currency crises.

Finally, investors tend to move away from the dollar when the US economy is slowing relative to the rest of the world. In recent years, the US has been growing significantly faster than the median rate for other developed economies, but it is poised to grow slower than its peers in coming years.

If the dollar is close to entering a downswing, the question is whether that period lasts long enough, and goes deep enough, to threaten its status as the world’s most trusted currency.

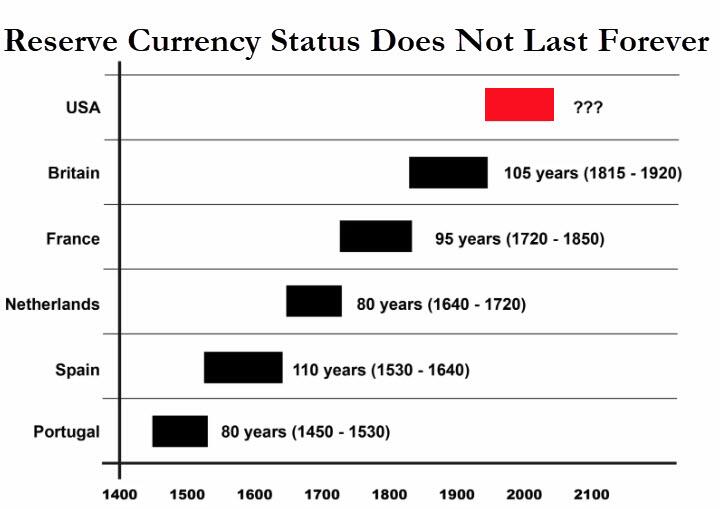

Since the 15th century, the last five global empires have issued the world’s reserve currency — the one most often used by other countries — for 94 years on average. The dollar has held reserve status for more than 100 years, so its reign is already older than most.

The dollar has been bolstered by the weaknesses of its rivals. The euro has been repeatedly undermined by financial crises, while the renminbi is heavily managed by an authoritarian regime. Nonetheless, alternatives are gaining ground.

Beyond the Big Four currencies — of the US, Europe, Japan and the UK — lies the category of “other currencies” that includes the Canadian and Australian dollar, the Swiss franc and the renminbi. They now account for 10 per cent of global reserves, up from 2 per cent in 2001.

Their gains, which accelerated during the pandemic, have come mainly at the expense of the US dollar.

The dollar share of foreign exchange reserves is currently at 59 per cent – the lowest since 1995.

Digital currencies may look battered now, but they remain a long-run alternative as well.

Meanwhile, the impact of US sanctions on Russia is demonstrating how much influence the US wields over a dollar-driven world, inspiring many countries to speed up their search for options. It’s possible that the next step is not towards a single reserve currency, but to currency blocs.

South-east Asia’s largest economies are increasingly settling payments to one another directly, avoiding the dollar. Malaysia and Singapore are among the countries making similar arrangements with China, which is also extending offers of renminbi support to nations in financial distress. Central banks from Asia to the Middle East are setting up bilateral currency swap lines, also with the intention of reducing dependence on the dollar.

Today, as in the dotcom era, the dollar appears to be benefiting from its safe-haven status, with most of the world’s markets selling off. But investors are not rushing to buy US assets. They are reducing their risk everywhere and holding the resulting cash in dollars.

This is not a vote of confidence in the US economy, and it is worth recalling that bullish analysts offered the same reason for buying tech stocks at their recent peak valuations: there is no alternative. That ended badly. Tina is never a viable investment strategy, especially not when the fundamentals are deteriorating.

So don’t be fooled by the strong dollar. The post-dollar world is coming.

* * *

The writer is chair of Rockefeller International

Authored by Ruchir Sharma, op-ed via The Financial Times,

Join: 👉 https://t.me/acnewspatriots

The opinions expressed by contributors and/or content partners are their own and do not necessarily reflect the views of AC.NEWS

Disclaimer: This article may contain statements that reflect the opinion of the author. The contents of this article are of sole responsibility of the author(s). AC.News will not be responsible for any inaccurate or incorrect statement in this article www.ac.news websites contain copyrighted material the use of which has not always been specifically authorized by the copyright owner. We are making such material available to our readers under the provisions of “fair use” in an effort to advance a better understanding of political, health, economic and social issues. The material on this site is distributed without profit to those who have expressed a prior interest in receiving it for research and educational purposes. If you wish to use copyrighted material for purposes other than “fair use” you must request permission from the copyright owner. Reprinting this article: Non-commercial use OK. If you wish to use copyrighted material for purposes other than “fair use” you must request permission from the copyright owner.

Disclaimer: The information and opinions shared are for informational purposes only including, but not limited to, text, graphics, images and other material are not intended as medical advice or instruction. Nothing mentioned is intended to be a substitute for professional medical advice, diagnosis or treatment.

![Tucker Carlson Released an ALARMING Message … [Published Yesterday]](https://ac.news/wp-content/uploads/2024/04/download-3-120x86.jpg)

Discussion about this post